Vacation Rental Income Tax Rules Explained: What Property Owners Need to Know in 2026

Updated January 31, 2026

Tax questions come up constantly in conversations with the owners we work with in Vail, Beaver Creek, and Sedona. At what point does rental income become taxable? What can we deduct? What happens if we use the home ourselves? These are reasonable questions, and the answers are specific enough that getting them wrong costs real money.

This post covers the core IRS rules that apply to most vacation rental owners, updated for 2026. One important note upfront: I am not a tax advisor, and nothing here should replace a conversation with a CPA who has short-term rental experience. What I can do is help you walk into that conversation knowing what questions to ask.

The Quick Reference

The 14-Day Rule: Where the IRS Line Begins

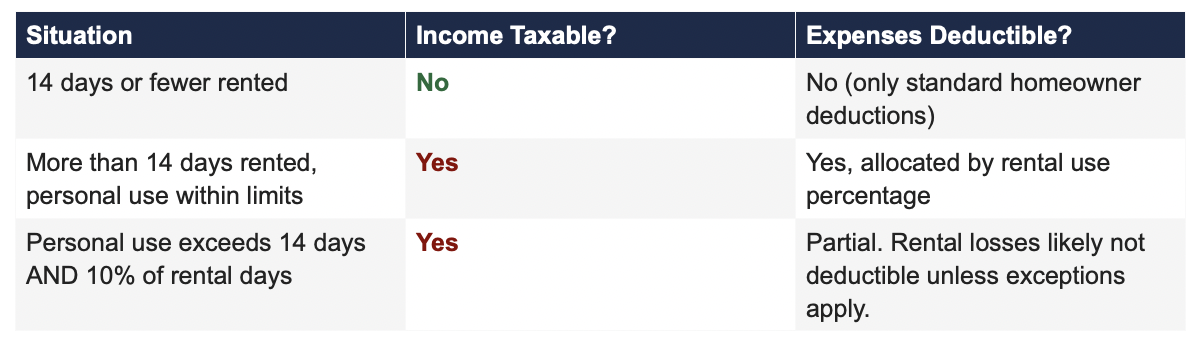

Rent your property for 14 or fewer days per year and the IRS does not require you to report that income at all. You owe nothing on it, and you cannot deduct rental-related expenses (other than what you would normally claim as a homeowner, like mortgage interest or property taxes on Schedule A).

On day 15, the IRS treats you as operating a rental business. Every dollar earned becomes taxable, all expenses must be documented and allocated, and personal use must be carefully tracked.

A note on intent: some owners try to stay under 14 days by blocking availability or limiting bookings after hitting the threshold. The IRS may look at your availability calendar and marketing activity alongside the actual rental count. Limiting bookings purely for tax avoidance is not a strategy that holds up well on examination.

Personal Use: How It Affects Your Deductions

The IRS defines personal use more broadly than most owners expect. Any day you or a family member stay at the property counts, even at full market rate. Any day you allow friends or family to stay for free or below market value counts. A day you spend at the property cleaning or doing maintenance counts as personal use unless you can document it was exclusively for necessary work and you received no personal benefit from the stay.

The threshold that matters

Personal use must stay at 14 days or fewer, or below 10% of total days rented, whichever is greater, to preserve full deductibility of rental losses.

Exceed that threshold and the IRS treats the property as a personal residence. You can still deduct a portion of expenses, but rental losses generally cannot offset other income unless your adjusted gross income is under $100,000 (with a phase-out through $150,000) or you qualify as a real estate professional.

A practical example: you rent the property for 100 days and use it personally for 15. Because 15 exceeds both 14 days and 10 percent of rental days (10 days), you have crossed the threshold and will likely be limited in your ability to deduct losses unless another exception applies.

Expense Allocation: What You Can Actually Deduct

Once your property qualifies as a rental, expenses fall into two categories.

Direct rental expenses

Costs that apply exclusively to the rental activity, such as cleaning fees between guest stays, platform listing fees, booking commissions, and guest supplies, are 100 percent deductible.

Mixed-use expenses

Costs that benefit both rental and personal use, such as utilities, insurance, mortgage interest, and property taxes, must be allocated. The formula is straightforward: divide rental days by total occupied days (rental plus personal). Vacant days do not count in this calculation.

Example: you rent 120 days and use the property personally for 30 days. That gives you 120 divided by 150, or 80 percent rental use. You can deduct 80 percent of mixed-use expenses on Schedule E. The remaining 20 percent of mortgage interest and property taxes may still be deductible on Schedule A, subject to standard limits.

Depreciation: The Deduction That Comes With a Catch

When your property qualifies as a rental, you are required to depreciate the building portion over 27.5 years. This is a meaningful annual deduction, and most owners should be taking it.

The catch is depreciation recapture. When you sell the property, the IRS taxes the depreciation you claimed at up to 25 percent, even if you did not actually claim it on prior returns. The IRS assumes you did. Skipping depreciation to avoid recapture does not work and leaves you with a worse outcome.

For owners with higher income or a long hold on a valuable property, a cost segregation study can accelerate depreciation by reclassifying certain components, such as appliances, flooring, and fixtures, from 27.5 years to 5 to 7 years. This front-loads the deduction significantly. Whether it makes sense depends on your income level, tax situation, and how long you plan to hold the property. A CPA with short-term rental experience can run the numbers.

Real Estate Professional Status

If you qualify as a real estate professional under IRS rules, rental losses can offset any income, including W-2 wages, with no passive loss limitations. The qualification requirements are specific: you must spend 750 or more hours per year in real estate activities, and real estate must represent more than 50 percent of your total working time.

Most owners with full-time jobs outside real estate will not qualify. Even licensed real estate agents often fall short if they are not also materially participating in the day-to-day management of the rental property, not just holding a license.

If you do not qualify as a real estate professional, you may still be able to deduct up to $25,000 in rental losses per year if you actively participate in managing the property and your AGI is under $100,000. That allowance phases out completely at $150,000.

The 1099-K Rules for 2026: A Correction Worth Reading

There has been significant confusion about 1099-K reporting requirements over the past few years, including in an earlier version of this post. Here is the current, accurate picture.

The IRS spent several years attempting to lower the 1099-K reporting threshold from $20,000 to $600. After repeated delays and significant pushback, Congress reversed course entirely. Following the passage of the One Big Beautiful Bill, the threshold has returned to $20,000 in payments and at least 200 transactions on a single platform for 2025 income and beyond. The $600 threshold that was widely reported as coming in 2026 will not take effect.

What this means in practice: most vacation rental owners will not receive a 1099-K from Airbnb or VRBO unless they exceed $20,000 and 200 bookings on a single platform in a calendar year.

The more important point, which has not changed, is that all rental income is taxable regardless of whether you receive a form. The 1099-K threshold only determines when a platform is required to report to the IRS. Your reporting obligation is not contingent on receiving one.

When you do receive a 1099-K, it reports gross payments, not taxable income. Fees, refunds, and cancellations are typically not netted out. You will need your own records to calculate actual taxable income, which is another reason clean bookkeeping matters throughout the year.

State and Local Tax Obligations

Federal income tax is only part of the picture. Most states and many localities impose occupancy or lodging taxes on short-term rentals, and the rules vary significantly by location.

Arizona requires owners to hold a Transaction Privilege Tax license and remit both state and local taxes. Sedona now also requires a local STR license. Platforms like Airbnb collect and remit some of these taxes in Arizona, but owners remain responsible for compliance and proper filing.

Colorado has state sales tax obligations for short-term rentals, and local lodging taxes vary by municipality. Vail and Beaver Creek both have local lodging tax requirements that owners should understand.

California limits certain short-term rental deductions and has specific income tax treatment for rental activity.

Hawaii imposes a general excise tax that applies to short-term rental income.

Do not assume that because a platform collects and remits some taxes, you are fully covered. Licensing requirements, local filings, and income tax obligations may still fall to you. Verify with a local tax professional in each state where you own rental property.

Documentation: What the IRS Expects

If you are audited, the burden of proof is on you. Vague records and missing receipts are the most common reasons owners lose deductions they were entitled to claim. The IRS expects receipts, not just credit card statements. It expects written logs of rental versus personal use days. It expects clear documentation of the business purpose behind every deduction.

The practical habits that make this manageable:

Use a dedicated bank account and credit card for all rental-related income and expenses

Use calendar software or your property management system to log every rental stay and every personal use day in real time, not reconstructed at year end

Keep receipts for every maintenance, repair, and supply purchase, however small

Document any day you visit the property for maintenance purposes with a written note of what was done

When to Bring in a Tax Professional

Some situations are straightforward enough that a well-organized owner can handle them with good accounting software and a general CPA. Others call for someone with specific short-term rental expertise.

Worth getting specialized help if you own multiple properties, have rentals in more than one state, have made significant capital improvements, are evaluating a cost segregation study, are unsure whether you qualify for real estate professional status, or have had inconsistent deduction practices in prior years that may need to be corrected.

When you are evaluating a tax professional, ask directly how they handle mixed-use property allocations, passive activity loss rules, and state-specific short-term rental tax obligations. A general preparer who has not worked with STR owners before may miss deductions or create compliance problems that cost more to fix than the original advice was worth.

Questions about how this applies to your property?

We are not tax advisors, but we work closely with owners navigating these rules every season and can connect you with professionals who specialize in short-term rental taxation. Reach us at +1 (970) 919-0243.

Garth Yettick is a co-founder of Luxart Property Management, which manages a curated portfolio of luxury vacation rental and second-home care properties in Sedona, Arizona and the Vail Valley, Colorado. This post is for informational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance specific to your situation.